Recently I met with the CEO of a Fortune 500 financial services company about something that was keeping him “up at night.” He said that while he has plenty of access to financial capital, thanks to flush markets and eager investors, he is extremely worried about his ability to access sufficient human capital to grow his business. “My number one job,” he said, “is to get talent to run my business—period.”

Recently I met with the CEO of a Fortune 500 financial services company about something that was keeping him “up at night.” He said that while he has plenty of access to financial capital, thanks to flush markets and eager investors, he is extremely worried about his ability to access sufficient human capital to grow his business. “My number one job,” he said, “is to get talent to run my business—period.”

CEOs across the country, and across industries, are experiencing similar anxiety. In a knowledge-based economy with an aging workforce and a slowing birthrate—not just in the U.S. but also around the globe—leaders face a perfect storm when it comes to talent acquisition and retention.

I really am not being hyperbolic when I say that, as CEOs, this is the challenge of our time. Because for all the talk about the worries over digitization, transformation and disruption, the best-laid plans to address those issues can be derailed by failures in talent acquisition and talent retention. Say, for example, your team develops an innovative new product that promises to take the market by storm. You have a 12-month calendar for roll-out. Suddenly, you learn that a competitor has poached your star brand manager tasked with taking your product to market. Now, you’re going to spend 60 to 90 days finding a replacement with the right technical skills and cultural fit/alignment—and then you have to get that individual up to speed. You’ve lost a critical four to five months in a 12-month window, derailing two years of planned growth that should have come from that new product—which is now at risk for obsolescence before it even hits the shelves.

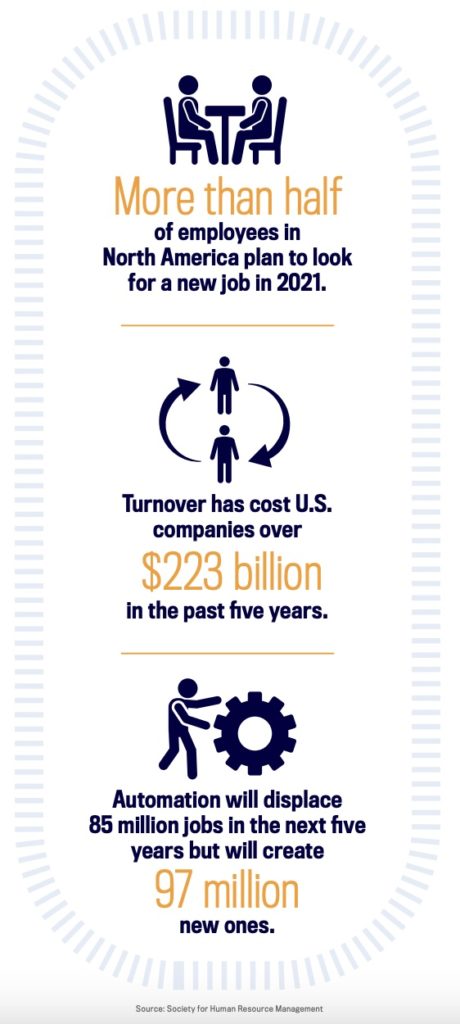

And the turnover tsunami is real. Yes, 30 percent annual turnover might just be the new norm. That is partly thanks to the pandemic, which gave people a year-plus to reflect on what they’re doing, whether it’s truly fulfilling, and what else they might like to do with their lives, now that they’ve been spared a deadly disease.

The year of remote work has also made it a lot easier to court talent—and for other companies to court yours. Before last year, it would have been difficult, if not impossible, to imagine hiring a six-figure executive without ever personally meeting them; that has become standard practice in the post-Covid era. Meanwhile, unemployment continues to drop, which is heating the war for talent to epic levels.

The solution? We need to have people strategies that are every bit as sophisticated and complex as those we have for technology, sales and marketing, finance and so on. Your people strategy is what ensures that the organization not only survives but also thrives long term. If you have a business strategy that’s reliant on people, but you don’t have a serious people strategy, that’s a really big problem. People are an enterprise risk—they literally mean business—and CEOs and boards need to view them that way.

The solution? We need to have people strategies that are every bit as sophisticated and complex as those we have for technology, sales and marketing, finance and so on. Your people strategy is what ensures that the organization not only survives but also thrives long term. If you have a business strategy that’s reliant on people, but you don’t have a serious people strategy, that’s a really big problem. People are an enterprise risk—they literally mean business—and CEOs and boards need to view them that way.

Your people strategy should include:

1. Retention tools.

How do we take care of the people we have? What are the ways we’re assessing people? Investing in them? Developing them? How are we measuring all that and making sure our best people are happy in their roles and feeling motivated and appreciated?

It’s worth noting that the answer to retention is no longer simply more money and “making my people happy.” Employees themselves don’t even necessarily know what they want anymore. They ask for stuff, they get it, and they still leave. Time was, you could keep somebody thinking of leaving by giving them another 10 percent to 20 percent. Nowadays, the war is so serious, people are literally doubling salaries. The former CHRO of a major Silicon Valley company told me the company’s strategy when they want to retain someone is to give them so much money, “we dare any other company to beat us.” That’s fine for deep-pocketed tech companies, I said, but what about the rest of us? His answer: “That’s your problem.”

And it is. Tactics like that have led to salary escalation and wage inflation and to problems inside companies, because when you raise one person’s salary, you risk demoralizing your other valued people who are looking around, thinking, “Where’s mine?”

If you’re the CEO of a small-to-midsize company, you obviously can’t compete with the Googles in your industry, so your comprehensive talent strategy has to compensate, and you need to lead with your strengths. For example, you may need to take risks on people who may not be quite ready for the job but who’ve shown potential; they don’t have enough experience to land that plum Fortune 500 role, but you may be able to get them there with some careful grooming. You can tell them, “You can do things here you won’t be able to do anywhere else.”

2. Recruitment plan.

What is our strategy for replenishing people? How are we ensuring that we have the right pipelines in place to replace those who have retired or left for other opportunities? This is critical because, of course, you will lose people, regardless of how much you pay them or perks you offer.

The CEO of a logistics business can hope her trucks last longer than average, but they may not. So she needs her people to be proactively examining the fleet, checking mileage to see which trucks are vulnerable to breakdown, the one they’re most at risk of losing, and then ask, “What is our plan to replace this truck?” Similarly, you have to be constantly reviewing your top performers and future leaders, asking, “What is our plan to replace this person?”

We don’t like to do that because it makes people sound fungible. It sounds harsh—but it’s not. It’s reality. Some of your best people are going to leave and, if the first time you’ve contemplated that is the day they resign, you’re going to be in serious trouble. Just as hospitals have to have a backup plan if the electricity goes out, you need a backup plan for each of your high performers; and the moment the electricity goes out is hardly the time to head for the hardware store to purchase a new generator.

Your CHRO and his or her team should be keeping tabs on potential hires in the industry, holding a short list of possible replacements for key roles should the need arise. That way, you’re not reactively responding when someone announces their departure and then scrambling to fill the spot, but rather, you’ll have a roadmap already devised.

Put simply, the level of discipline, intentionality and focus you put on anything else in your business has to also be on your talent, which means a serious and comprehensive labor strategy that is not year to year, but rather proactively five to 10 years out.

3. The backup generator.

Your strategy should include not only a shortlist of candidates who might fill a role but other ways to tackle that need in the interim. This is where I often think of the people strategy as a “work strategy” because, after all, it’s the work that needs to be done; your employees are one way that work gets done, but they’re not the only way. So, what are the other ways to do the work? Those can be part of your toolbox, either to stop-gap the loss of a key role or to replace it, where appropriate. For example, if you lose your in-house counsel, your immediate thought is to go hire a new one. Not so fast. You should ask yourself whether you might be better to outsource that work to a law firm or use on-demand workers in platforms like Upwork.

And it may not be about finding new people at all to do the work. Maybe you should consider incorporating artificial intelligence, machine learning, robotics and other technology that can effectively do “the work.” Your in-house people, your contractors and outsource partners, and the technology you invest in are all part of your combined workforce. It’s HR’s job to figure out how they best fit together.

Ultimately, regardless of the industry, the talent war will be won by those companies that have a comprehensive work strategy that is proactive rather than reactive—and realistic rather than denial-fueled. In the same way we have to work with our boards to identify our potential successors—much as we hate the thought of letting go of the reins—we also need to be practical about our best people. And if we accept that no CEO can grow his or her business without the right human capital on board, we will elevate our people strategies so they get the attention, resources and visibility they deserve.